28 Things Economic Developers Need to Know This Week

April 30, 2026 edition

Welcome to this week's issue of What Economic Developers Need to Know This Week, where we collect links, charts, and ideas about the economy and place.

This week: 28 stories, graphics, and rabbit holes that are mostly relevant to economic development.

Today's email is brought to you by Resource Development Group

Resource Development Group and Convergent Nonprofit Solutions have recently announced a merger of these two well respected firms. RDG is now operating as Resource Development Group, a Convergent Company and will lead the combined operations in economic development and chamber engagements. Meanwhile, the Convergent banner will take the forefront on efforts on supporting traditional philanthropic and higher education organizations

This merger maintains RDG's innovative and custom approach while also creating the deepest bench of economic development and chamber fundraising expertise in the industry, the most complete data set in the country regarding economic development and chamber funding, and the greatest flexibility to be able to support engagement models tailored specifically to every market, regardless of size.

Whether you’re a single county EDO ready to kick off your first fundraising campaign or a large regional organization on your third funding cycle, they have the team and experience to get you the results you’re looking for.

1) Economic development and developers in the news #241: 85 economic development executives and organizations in 28 states. A fast scan of what they were sharing this week. Read: Economic Development and Developers in the News #241.

2) Podcast 216: The ecosystem now stretches well beyond city limits. Teresa Nortillo's conversation is a reminder that communities are competing through regions, partners, infrastructure, workforce, and execution capacity, not only through what sits inside one jurisdiction. Listen: Economic Development Isn't What It Used to Be with Teresa Nortillo.

3) 21 new economic development jobs this week: Roles in 14 states, from $37,000 to $168,000. A practical market check on who is hiring, where they are hiring, and what they are paying. Browse: 21 New Economic Development Jobs This Week.

4) Last week's 17 things issue: The April 23, 2026 catch-up link. Start here before you drop into the rest of this week's stack. Read: 17 Things Economic Developers Need to Know This Week.

The Econ Dev Show is brought to you by Sitehunt. Can you instantly score your sites against the next RFI? Sitehunt can. Book a demo.

5) Burnout is not a personal failure in economic development: Burnout is an organizational risk. In small teams, chronic overload affects project follow-through, board confidence, partner relationships, and staff retention. Read: Burnout Is Not a Personal Failure in Economic Development.

6) You didn't lose because of incentives: Delay, risk, and confusion are often the real competition. Price matters, but companies also care about certainty, permitting clarity, utility timing, decision speed, and whether the local process feels manageable. Read: You Didn't Lose Because of Incentives.

7) Rural economic development is now a full local systems job: Rural strategy is no longer just recruitment plus sites. It is housing, health care access, childcare, broadband, schools, utilities, entrepreneurship, downtown vitality, and the public capacity to make all of those pieces work together. Read: Rural Economic Development Is Now a Full Local Systems Job.

8) Building resilient economies through community-driven directories: Most communities still do not have a clean, current view of their own business base. A good local directory is business retention infrastructure, disaster response infrastructure, and a way to see supply chains, gaps, and hidden local strengths. Read: Building Resilient Economies Through Community-Driven Directories.

Stop managing sites in a spreadsheet disguised as a map.

Most tools help you store property listings and make them look good online. Sitehunt actually understands your sites. It pulls together infrastructure, utilities, zoning, and regional context from millions of real data sources to build a complete picture automatically. No manual data entry. No guessing. No chasing down answers when a project comes in.

When the RFI hits, speed wins. Sitehunt doesn’t just display your sites, it evaluates them. You can match properties to project requirements, answer detailed questions instantly, and move from “we think this might work” to “here’s exactly why it works” in minutes. While others are still assembling information, you’re already submitting a complete, confident response.

9) Should EDOs give a bonus incentive to target industries?: Should incentives reward strategic fit? Jim Gibson's prompt asks whether incentive policy should reflect a community's target sectors instead of treating every project the same.

10) The dying cities are winning the boomtowns: Growth rate alone can mislead. Some slower-growth or older industrial places have infrastructure, housing stock, lower costs, institutions, and political urgency that can become advantages when boomtowns run into affordability and capacity limits.

11) Permitting is now part of the site-selection product: Permitting is part of the product now. Buyers need to understand zoning, infrastructure, environmental review, political risk, and approval timing quickly enough to keep the project alive.

12) Manufacturing share still matters: Manufacturing concentration is not just a nostalgia metric. It shapes wages, supplier networks, training systems, local tax bases, transportation demand, energy demand, and the kinds of shocks a region can absorb.

13) South Carolina's freeway for bikes: A trail can be a real place-based asset. The Swamp Rabbit Trail works as transportation infrastructure, tourism infrastructure, small-business infrastructure, and quality-of-life infrastructure at the same time.

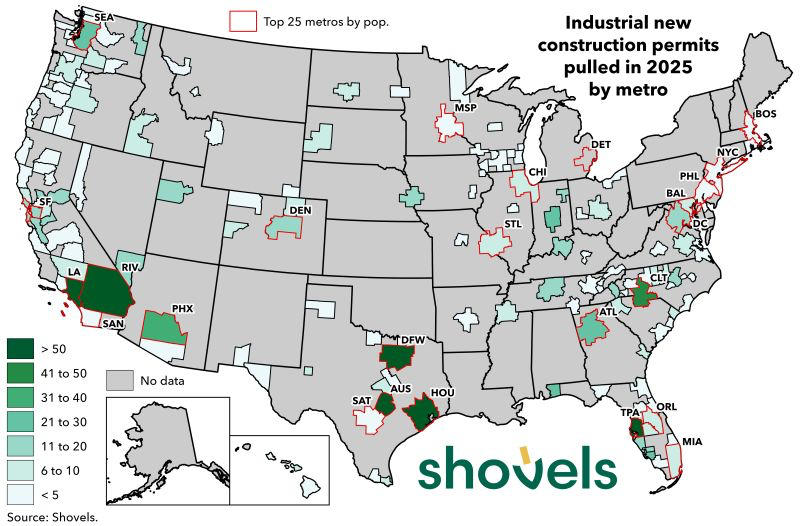

14) Industrial construction permits show where the work is moving: Actual industrial construction activity, not just announcements. Riverside, Dallas-Fort Worth, Houston, Phoenix, Charlotte, and parts of Florida stand out, which is another reminder that growth is concentrating around places that can convert demand into permitted projects.

15) Construction costs rarely fall: Waiting for costs to normalize is not a strategy. Brian Potter's construction-cost history matters for every housing, site-readiness, infrastructure, and downtown project. Communities need better process, smaller risk premiums, clearer approvals, and more buildable supply.

16) Economic development is an extrovert's game: Relationships still decide what turns into a project. Data and digital tools matter, but this work depends on trust, follow-up, informal information, and repeated contact.

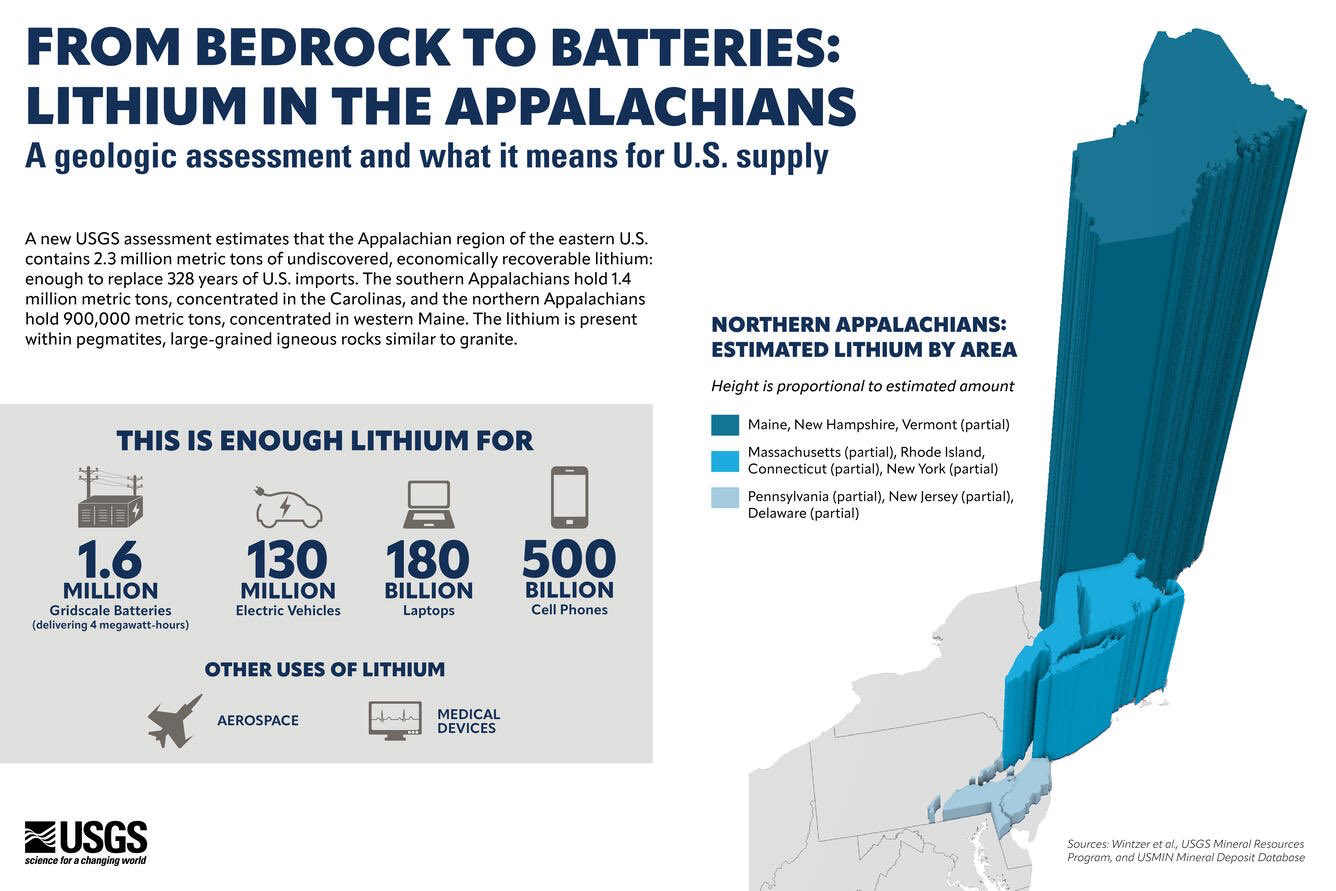

17) From bedrock to batteries: 2.3 million metric tons of economically recoverable lithium. The USGS estimate shown here puts 1.4 million metric tons in the southern Appalachians. The local question is whether geology can become processing capacity, workforce, permitting, roads, power, and local benefit.

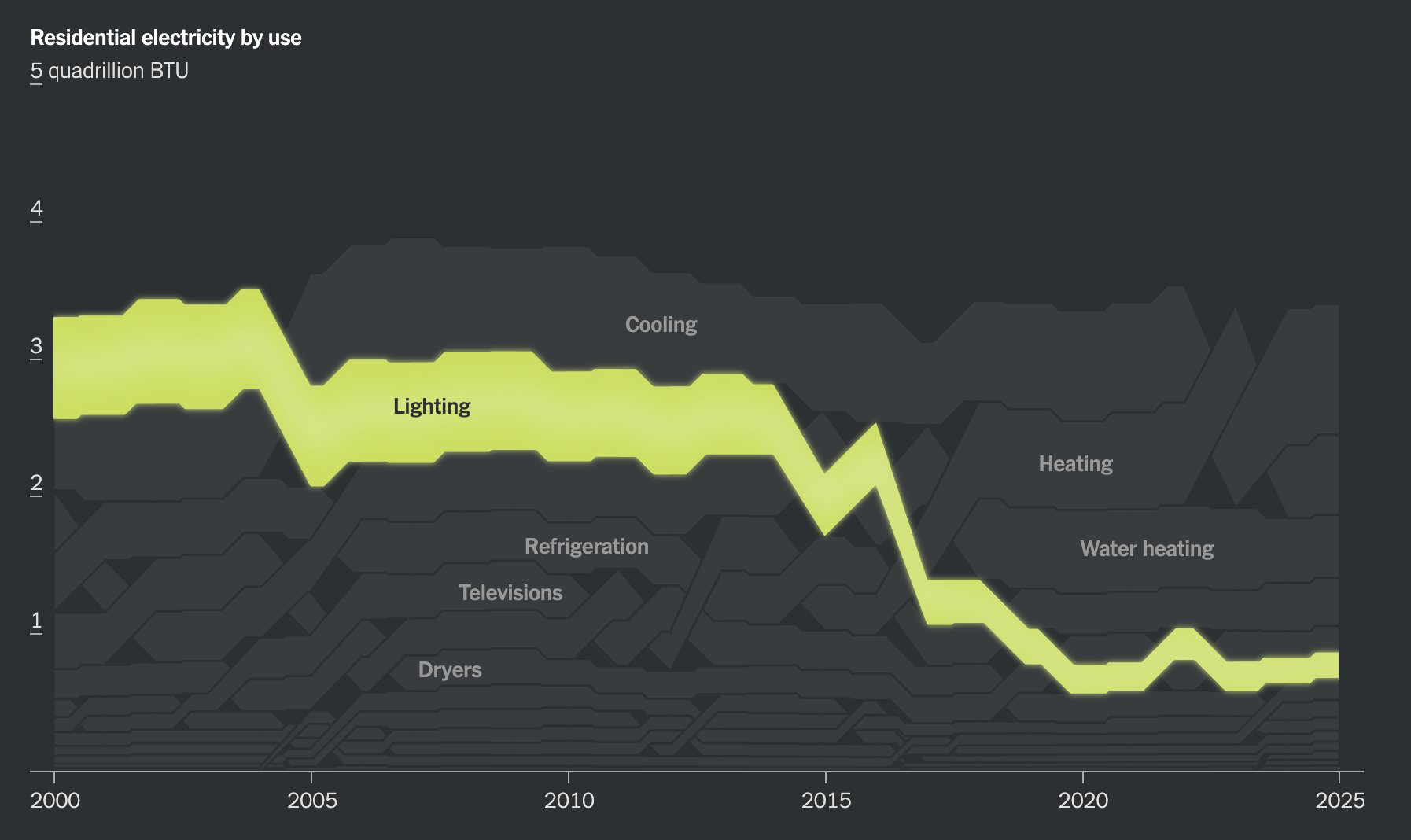

18) Residential electricity use has changed underneath the grid debate: Lighting fell from first to sixth in this chart. Efficiency can quietly reshape demand, but the next wave of load growth is coming from a very different mix of industrial, data-center, and electrification pressures.

19) Foreign-funded opposition to U.S. data center expansion: Data-center politics are now part of the site-readiness package. Whatever you think of the report's framing, community opposition now sits alongside power, water, land, and tax structure.

/

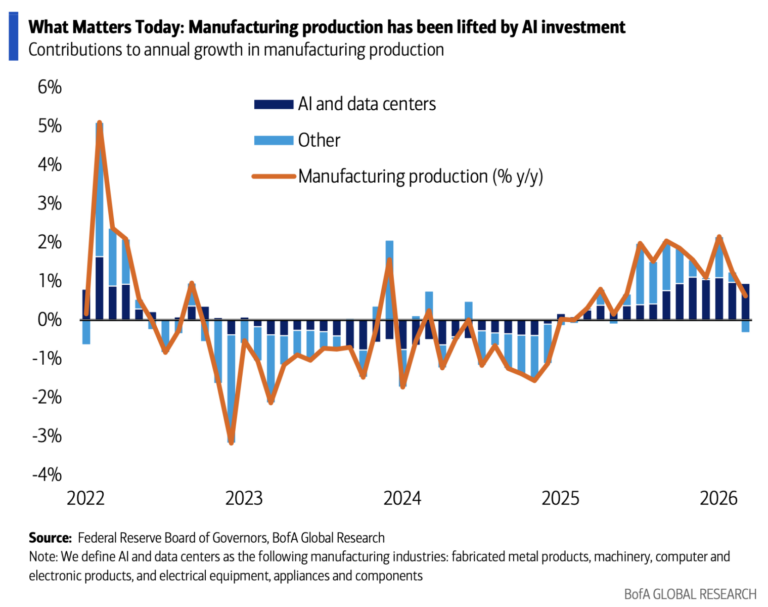

20) AI investment is showing up in manufacturing production: The AI buildout is also a physical supply-chain story. BofA's chart frames AI and data centers as a tailwind for manufacturing output, especially through fabricated metals, machinery, computer and electronic products, and electrical equipment.

21) Farmers are pairing solar panels with livestock: Agrivoltaics changes the local conversation. When solar projects can support grazing, land maintenance, and discounted electricity, communities have a different debate than they do around single-use energy projects.

22) The Jevons employment effect from AI: Cheaper professional work could expand the market for that work. If AI lowers startup costs and expands small-firm formation, the local entrepreneurship system becomes a bigger part of workforce strategy.

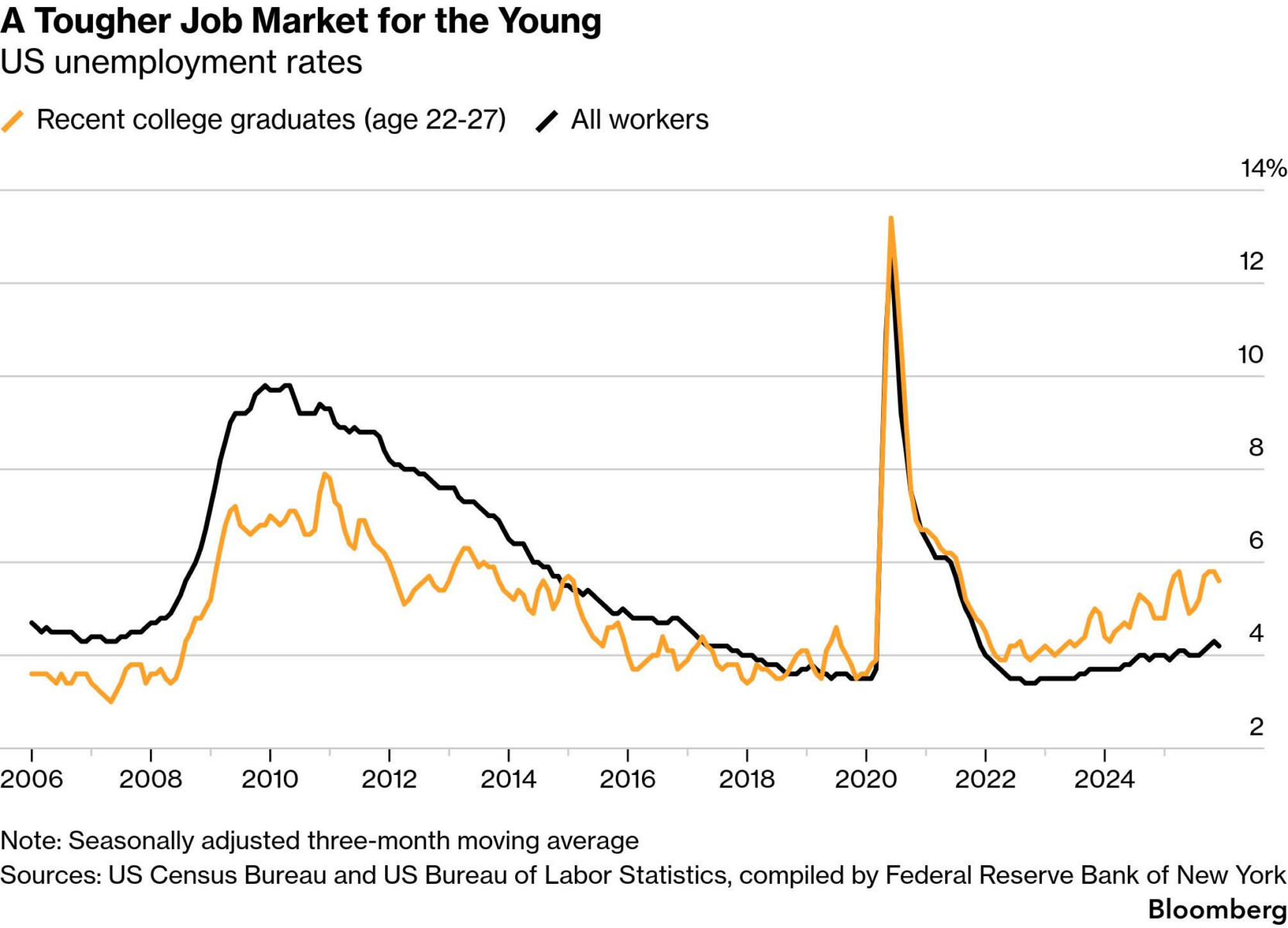

23) A tougher job market for young workers: Recent college graduates are facing a tougher labor market than the headline suggests. That matters for retention, downtown housing demand, early-career hiring, and whether young talent sees a reason to stay.

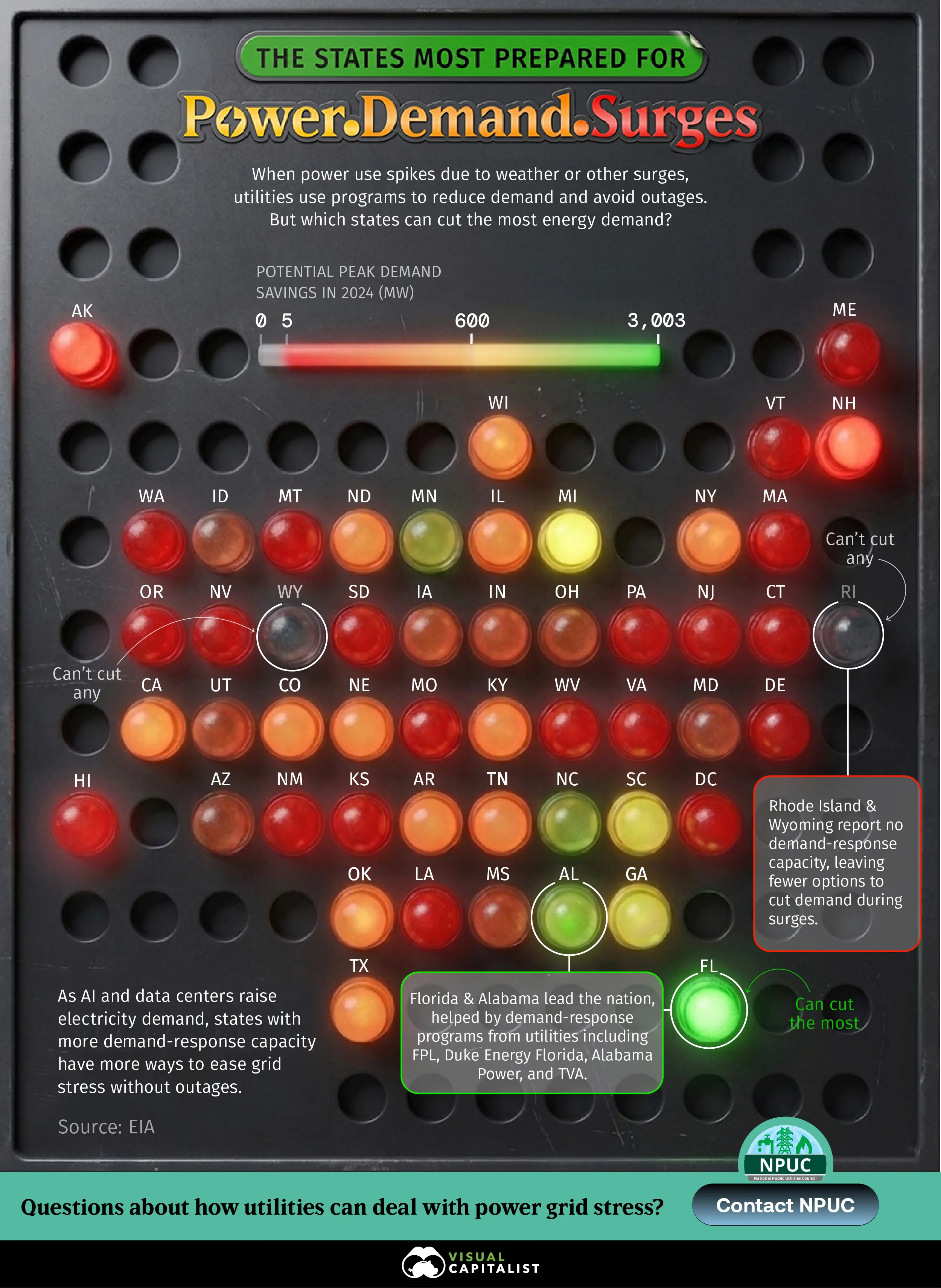

24) Some states are better prepared for power-demand surges: Megawatts are not all equal. Visual Capitalist's map highlights demand-response capacity, which is becoming more important as AI, data centers, weather events, and electrification put more stress on the grid.

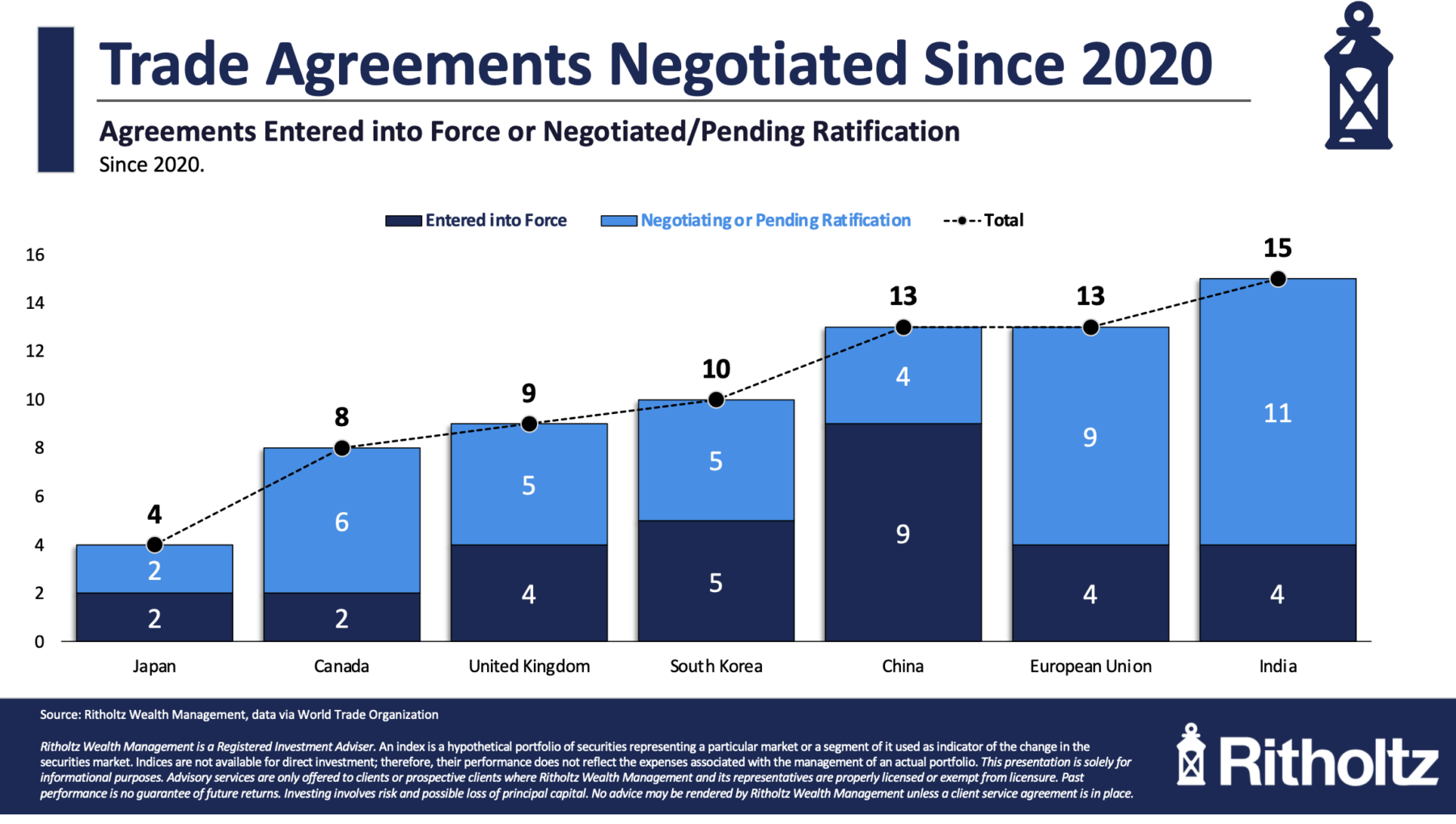

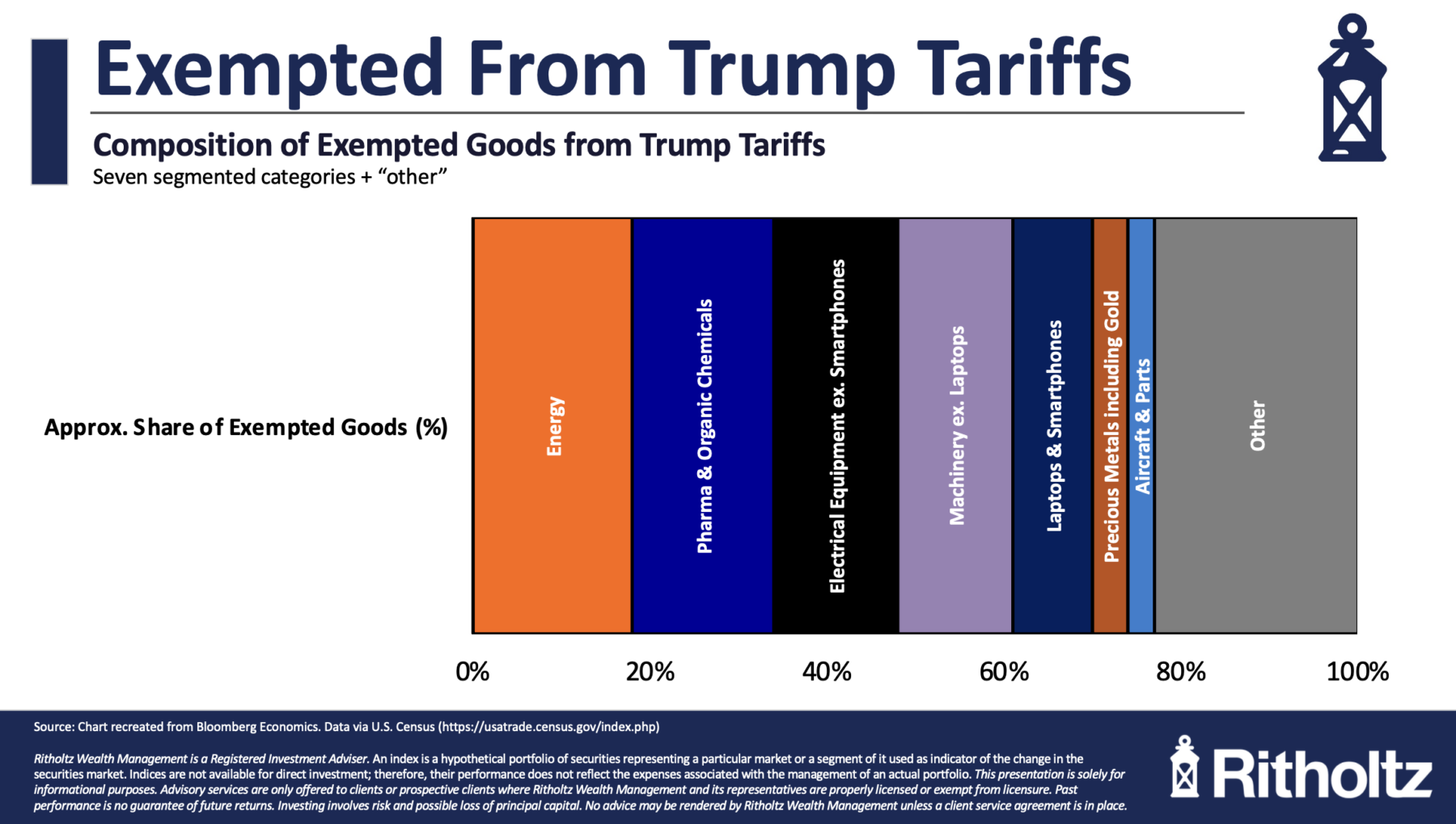

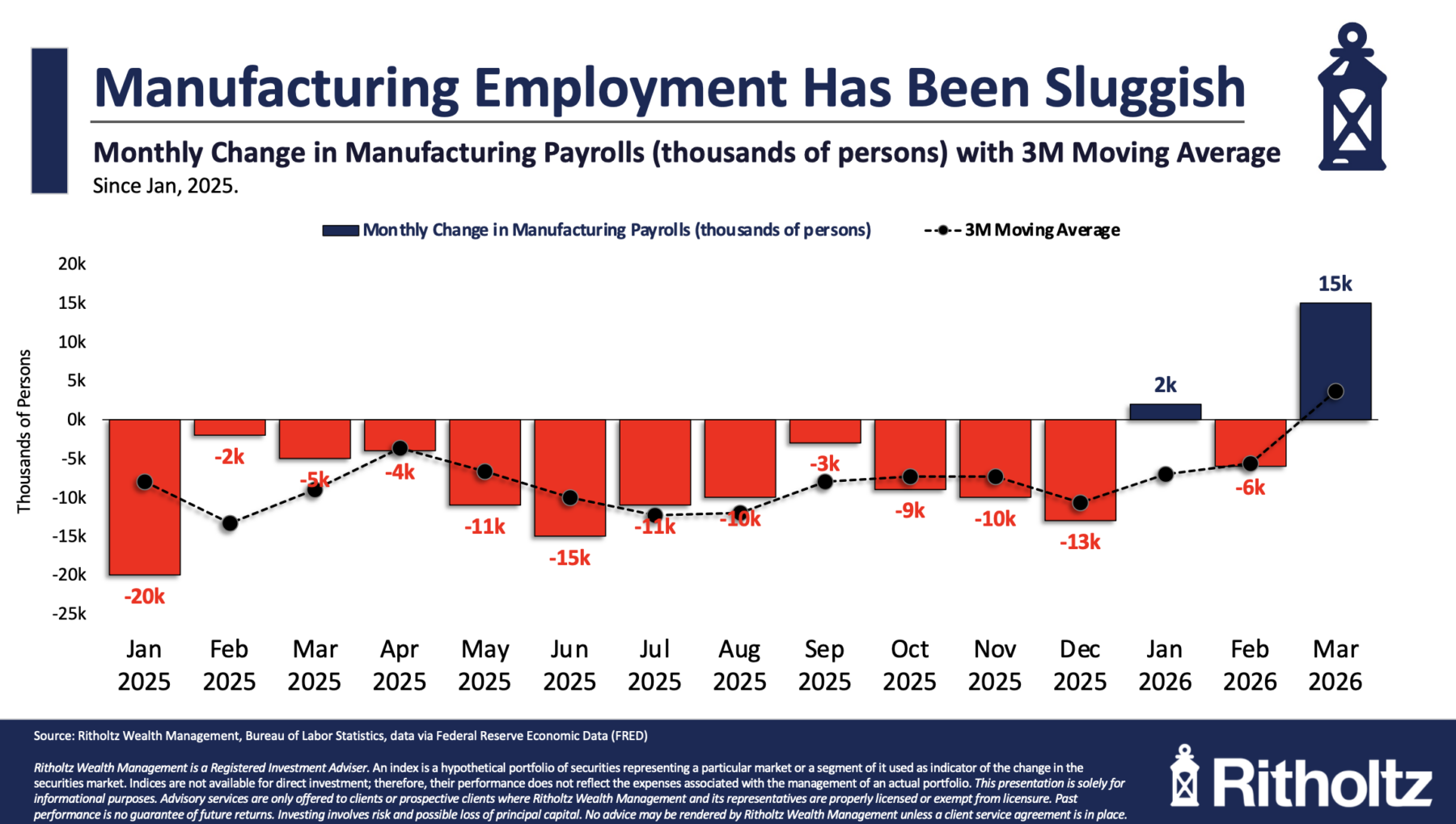

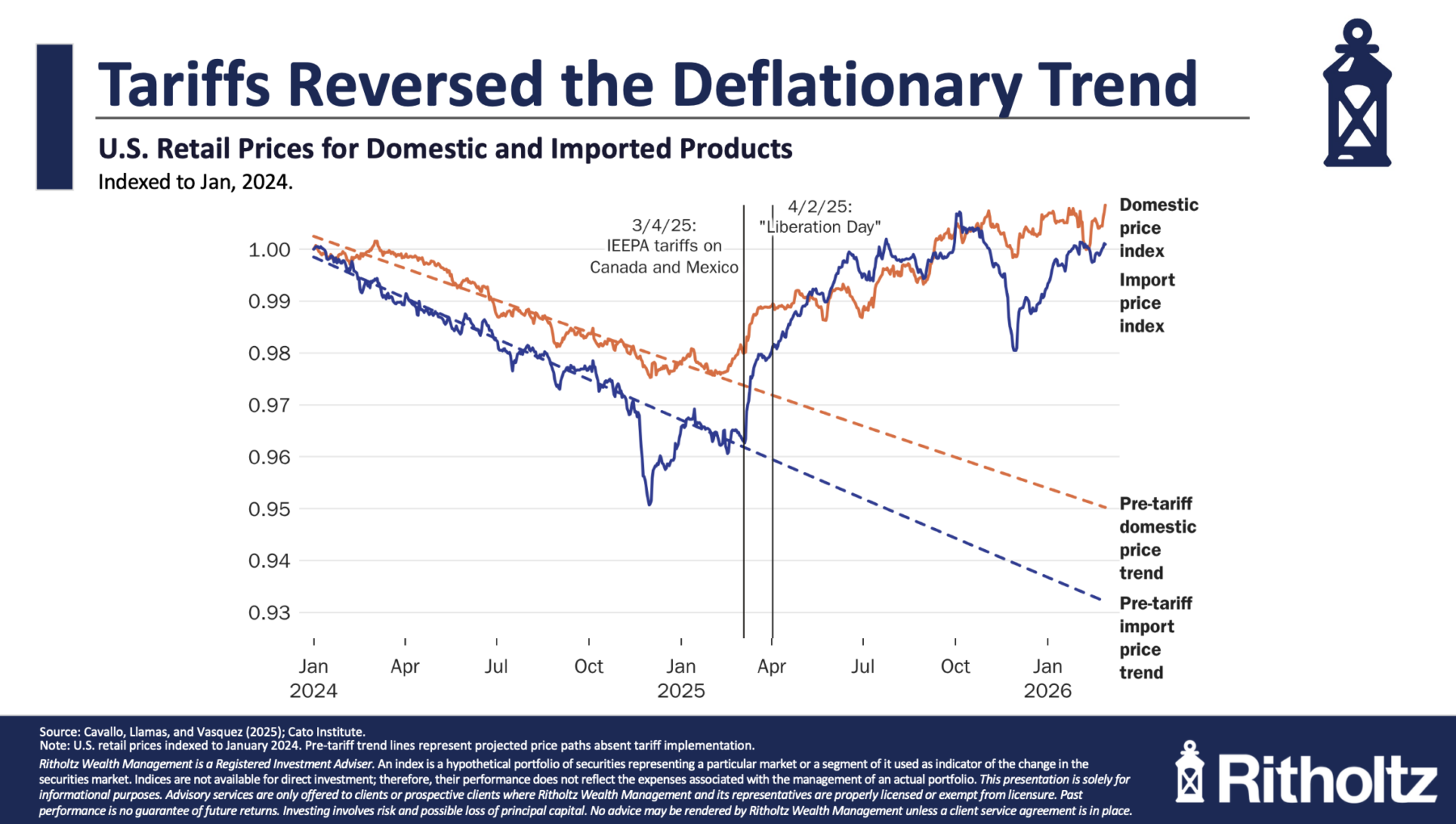

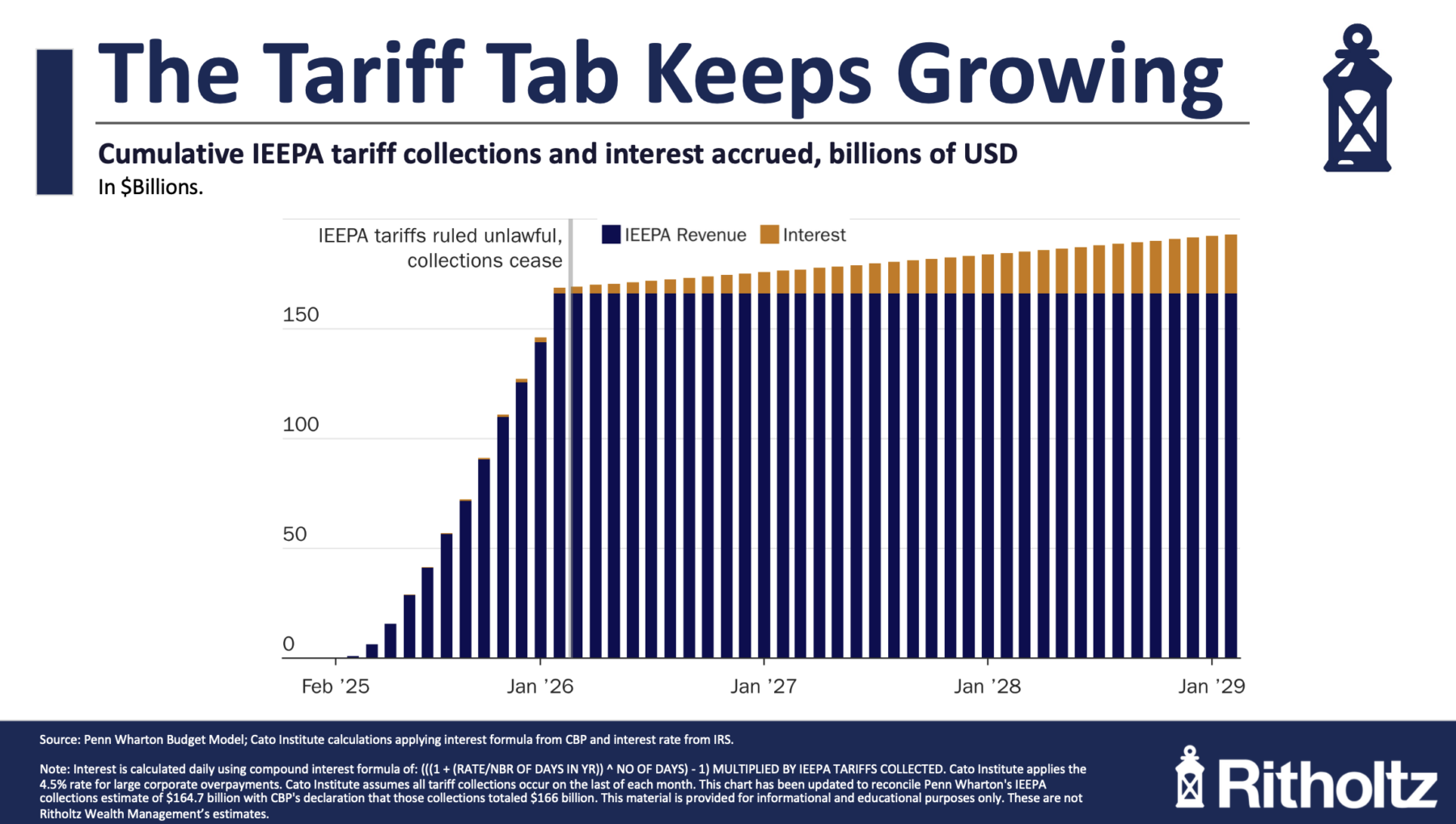

25) The tariff stack is getting more complicated: Tariff uncertainty affects supplier costs, site decisions, reshoring claims, retail prices, and capital-project confidence. This set of charts shows tariff policy from multiple angles at once: trade agreements, exemptions, manufacturing payrolls, retail-price effects, and cumulative collections.

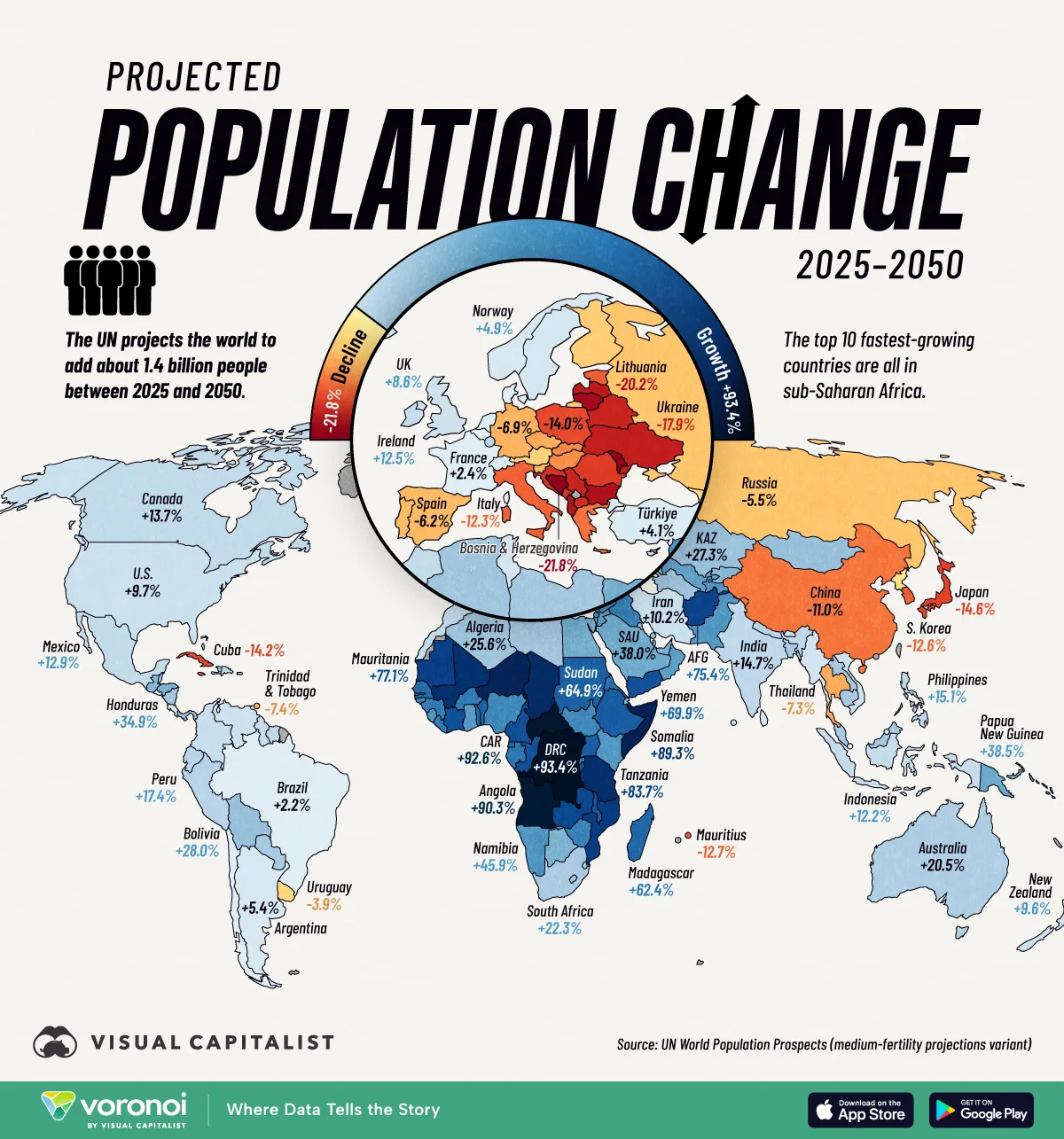

26) How the world's population will change by country: Demographic growth is shifting unevenly around the world. North America is projected to keep growing modestly, Mexico is shown at +12.9% from 2025 to 2050, and the fastest-growth countries are concentrated in sub-Saharan Africa.

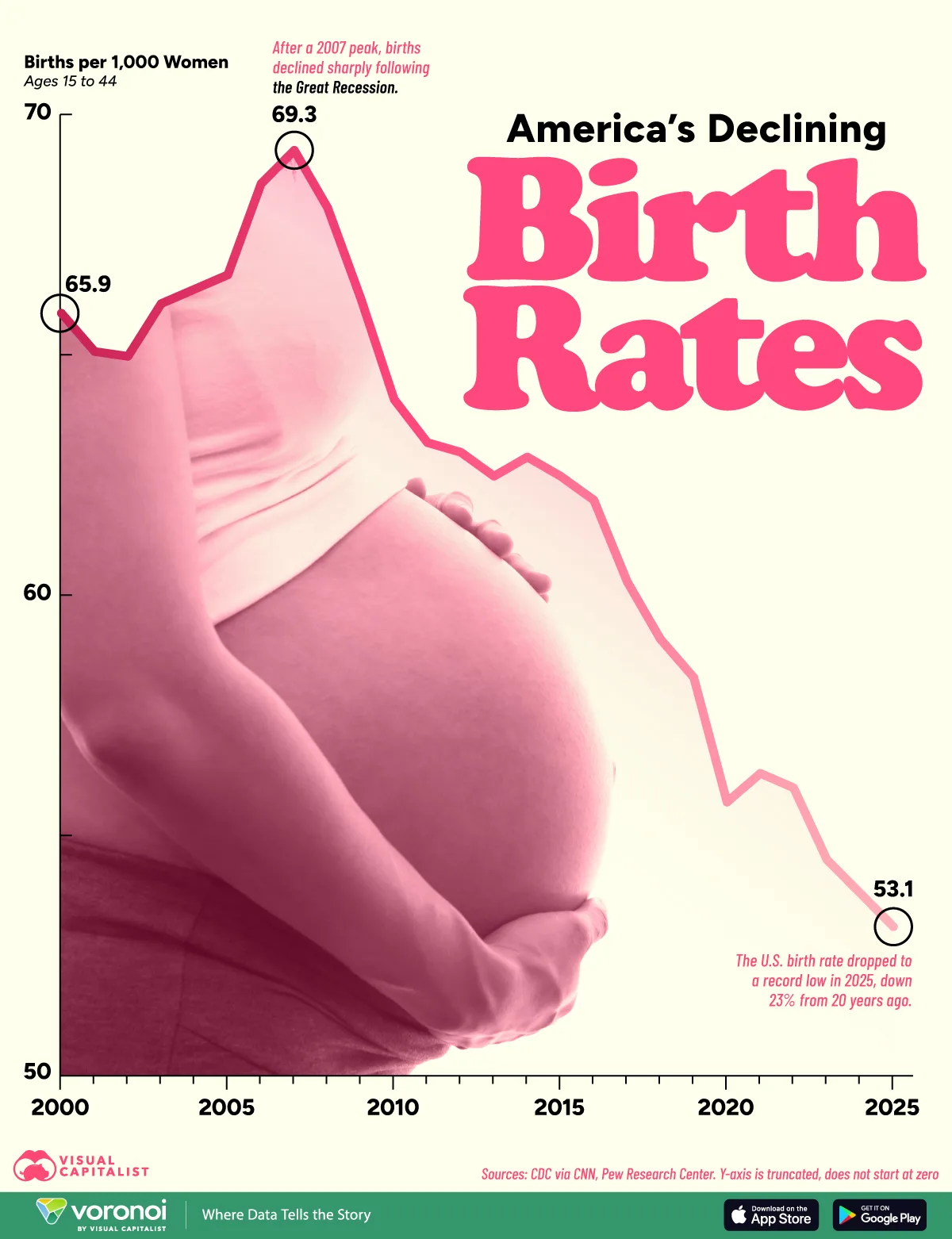

27) U.S. birth rates have not recovered from 2007: The fertility story is now a local economic-development story. Fewer births eventually flow into school enrollment, labor-force growth, housing demand, higher-ed pipelines, and the politics of public services.

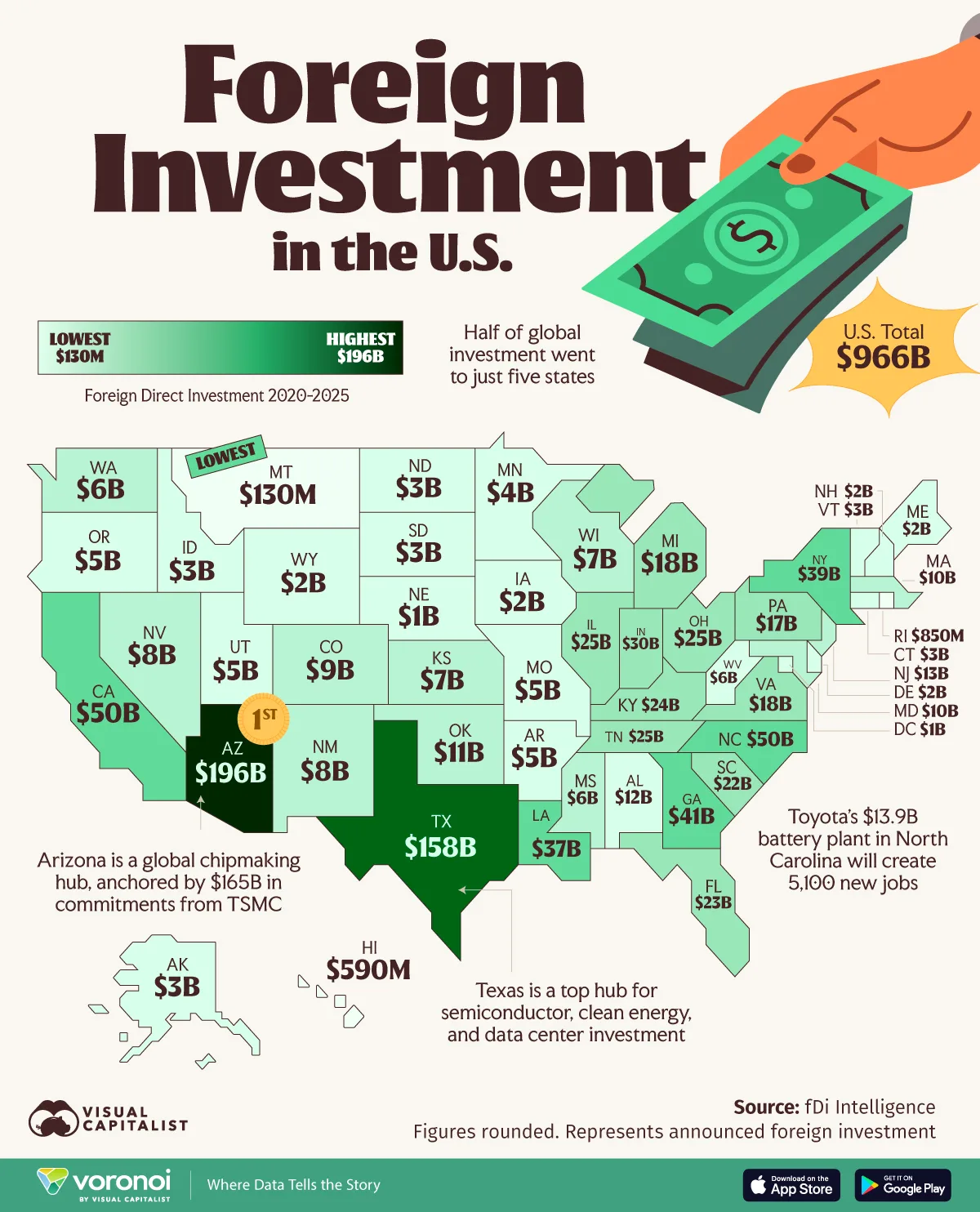

28) Foreign investment by U.S. state, 2020-2025: FDI is not a generic attraction category. It follows sector specialization, utility capacity, sites, supply chains, and confidence that a project can actually get built.